Building a resilient oxygen market in Nigeria

A map of supply and demand

Nigeria has made substantial investment in medical oxygen production over the last decade: more than 100 PSA plants installed and over 220 tonnes per day of liquid oxygen capacity on record. Yet access to oxygen at the point of care remains uneven.

In late 2025 and early 2026, the Oxygen CoLab worked with Primus Deus Consults to make visible the layer of the market that has been largely hidden from view: the small- and medium-sized oxygen suppliers whose work determines whether produced oxygen reaches the patients who need it.

Who did we engage?

140+

Suppliers verified

Operating medical oxygen suppliers confirmed across two waves of fieldwork

1500

Leads surfaced

Wholesalers, regional specialists, industrial SMEs, micro-distributors

80

SMEs assessed

SMEs that completed a full supplier profile

If you are working to improve oxygen access in Nigeria, these insights are for you.

Having a plant installed is not the same as having oxygen at the bedside.

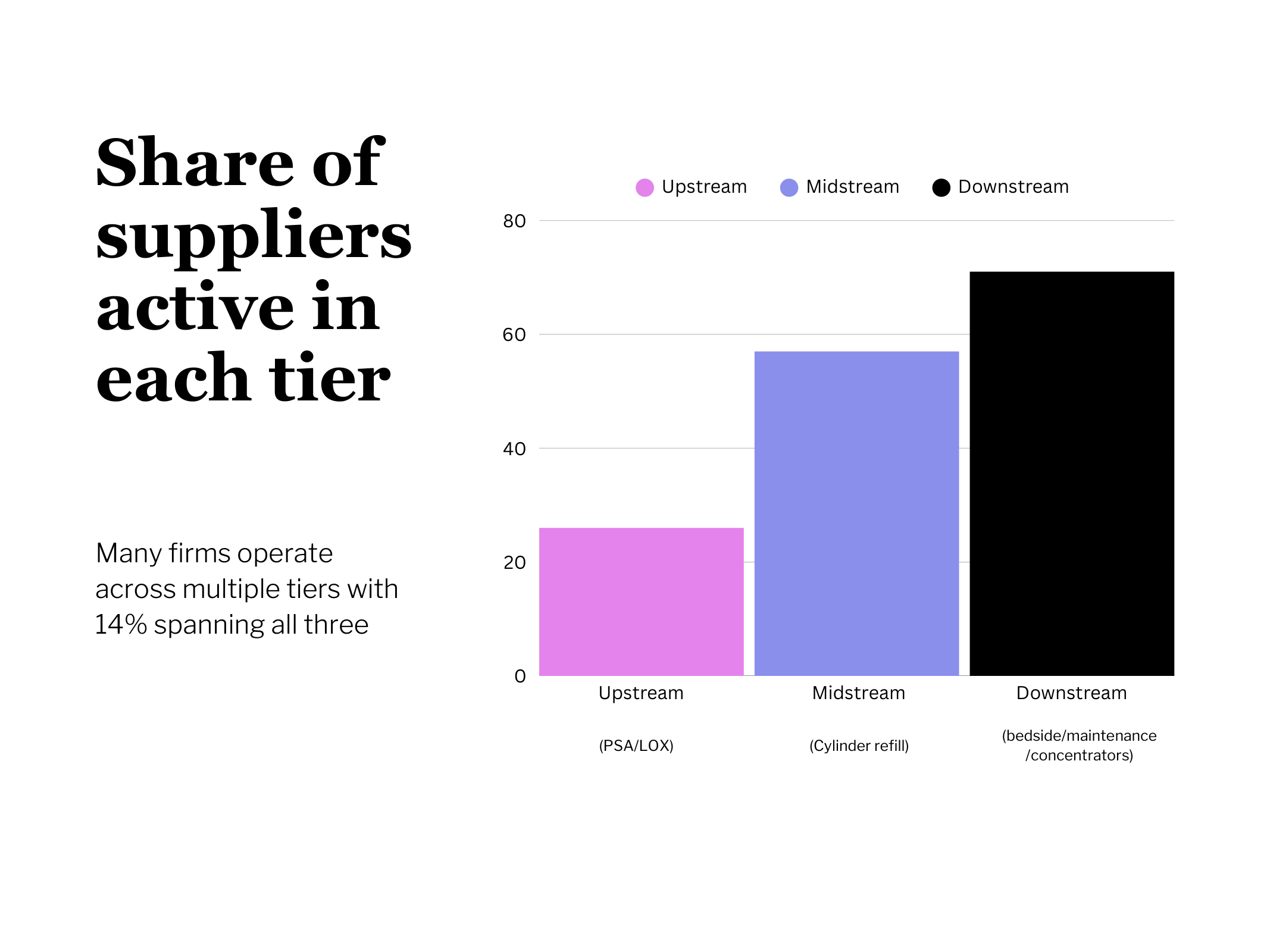

There is a Missing Middle

Nigeria's production capacity is well-documented. What this mapping reveals is a much larger, less-visible layer: the small- and medium-sized oxygen suppliers (SMEs) doing the work of moving, installing, maintaining and delivering produced oxygen to the point of care. They have been operating in Nigeria's oxygen market in larger numbers than has been recognised, and even this exercise still undercounts them: when we asked health facilities directly about their suppliers, most of the SMEs they named had not shown up in the nationwide scan; a sign the true market is materially bigger than any single mapping method can reach.

Oxygen SMEs are critical, but un-supported

Just 40% of suppliers report being reliably profitable, and the layer as a whole operates at the edge of what SMEs without outside capital can sustain. 60% rely entirely on their own capital to operate and grow. Only 11% have accessed commercial lending and under 5% have accessed development finance. Asked what would help them most, the answer comes back clearly and consistently from suppliers themselves

The capability gaps in the data are consistent with chronic under-resourcing rather than absence of ambition. Among the 53 SMEs physically handling oxygen equipment, 17% have no biomedical technician on staff and 32% document no preventive maintenance protocols. Among cylinder refillers, roughly a quarter rarely or never inspect returned cylinders before refill. This is a layer carrying a market-critical function on its own balance sheet, with almost no policy scaffolding or supportive commercial capital behind it.

77%

Place working capital financing in their top-3 support priorities

74%

Name market development through demand aggregation and procurement contracts as a top priority

69%

Name strategic partnerships with producers, distributors, and facilities as a priority

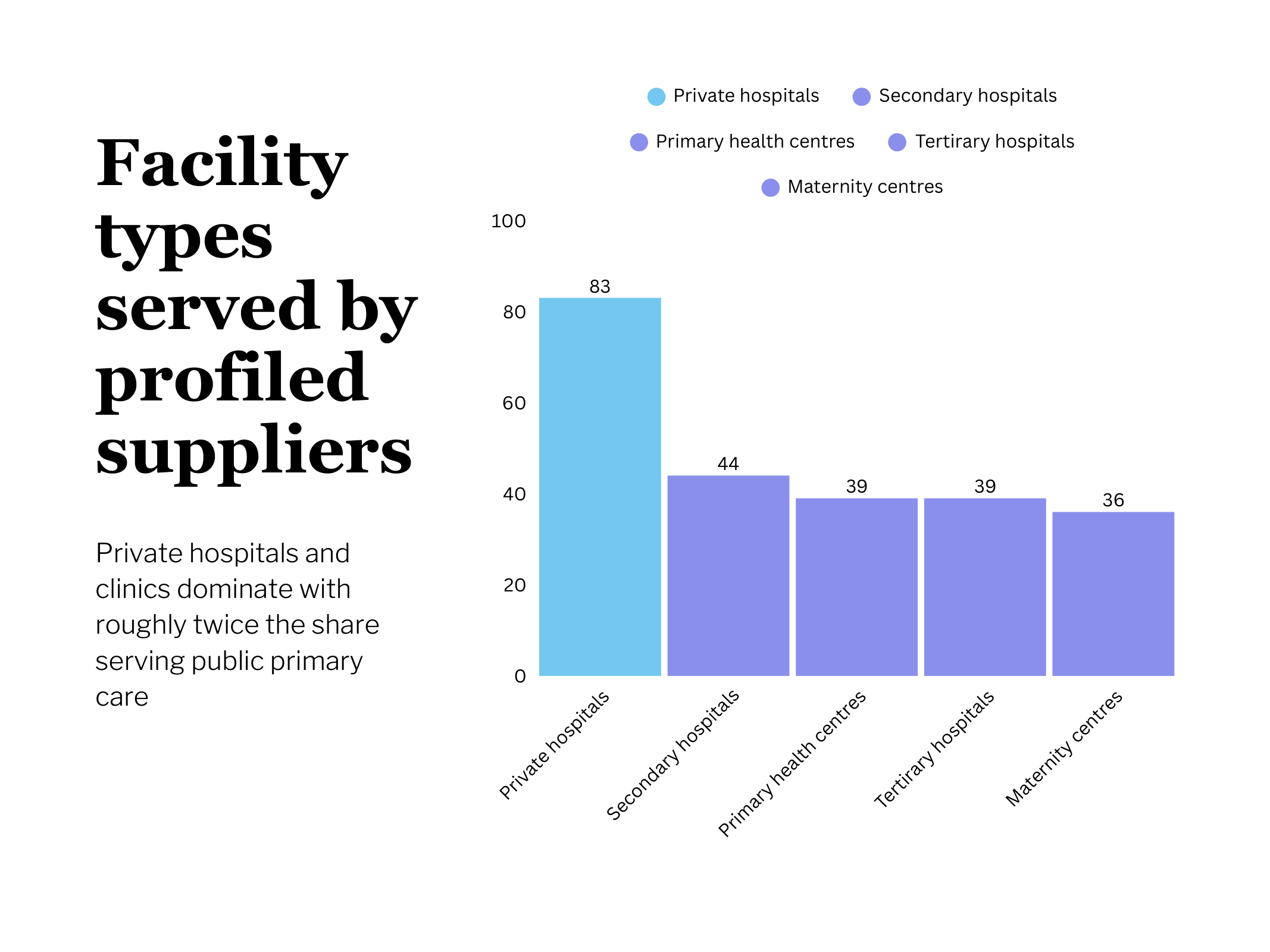

Surviving SMEs reflect market development

Of the SMEs profiled, 83% serve private hospitals and clinics, i.e., roughly twice the share serving public primary care or maternity centres.

33% name delayed payments from government facilities among their top financial risks

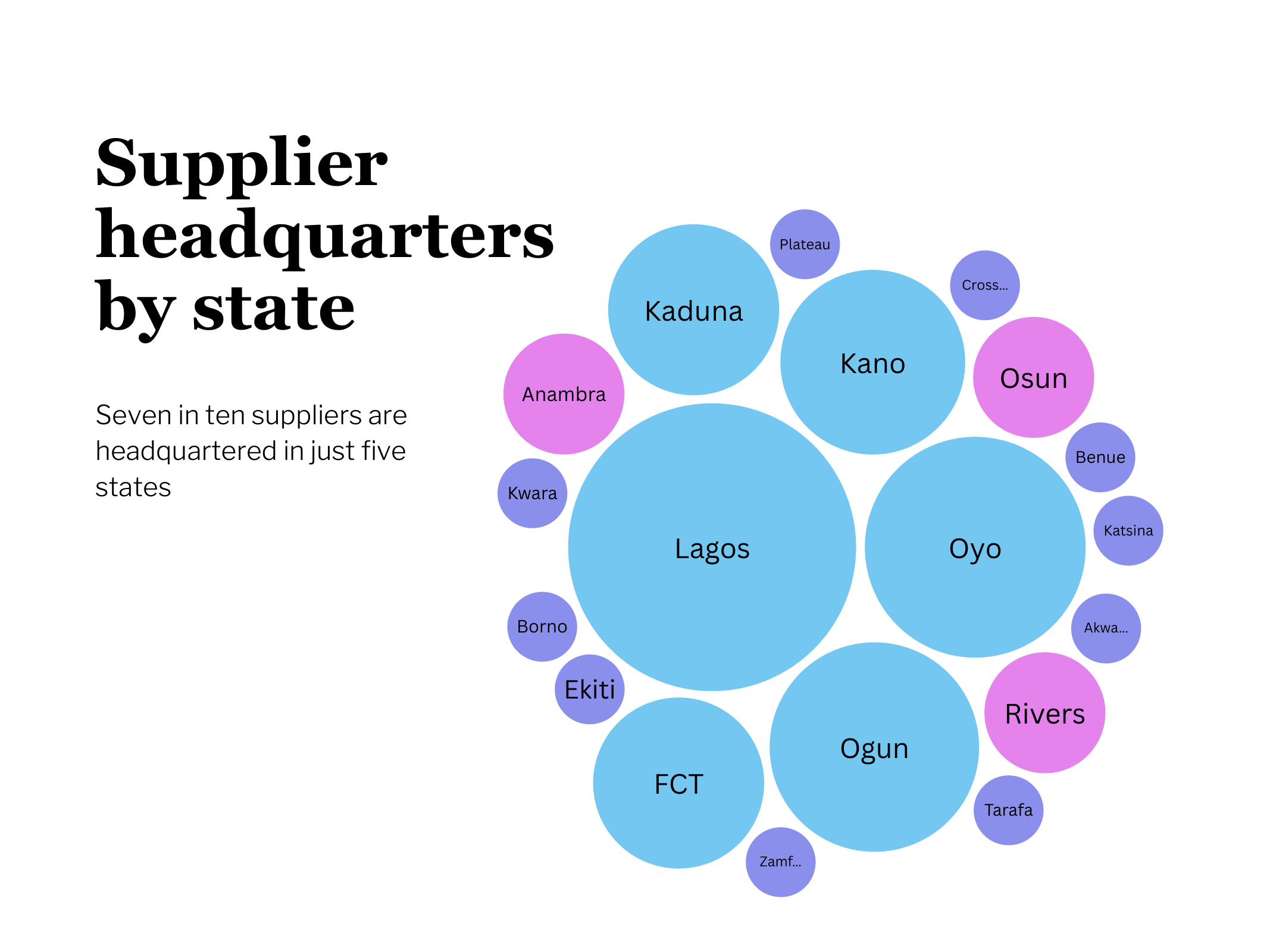

Seven in ten are headquartered in Lagos, Oyo, Ogun, Kano and Kaduna.

This is not simply a logistics gap. It reflects where market development is happening, shaped by purchasing power, infrastructure, and proximity to industrial supply chains.

For small, under-capitalised SMEs, delayed public payment and long delivery distances are not absorbable on their own balance sheets.

The regions with the highest unmet clinical need are therefore, in many cases, the regions with the fewest suppliers and the thinnest market activity.

Oxygen SMEs want to close the gap

Three-quarters of suppliers place working capital financing and market development, e.g. procurement certainty, and demand aggregation, at the top of the help they need. Roughly 7 in 10 name strategic partnerships with producers, distributors, and facilities.

A subset of SMEs are already profitable and actively seeking outside capital to grow. What they are asking for is the combination of patient capital, procurement certainty, and regulatory clarity that would let SMEs carrying a critical market function do it reliably and at scale.

The evidence from this mapping is clear: Nigeria's oxygen gap is the under-supported layer sitting between production and patients. Closing the gap depends on government setting the rules and by smart, private operators delivering reliably, and partners enabling the market.

Oxygen CoLab is working to build resilient local oxygen markets by tackling the barriers that stop supply from reaching patients: fragmented procurement, unclear regulation, under-supported SMEs, and invisible financing. Across these four areas, we are helping governments and suppliers create the conditions for reliable, investable oxygen services that can last beyond grant funding.

This report was prepared by Jason Houdek with data from Primus Deus Consults